Photovoltaic I: Polycrystalline Silicon

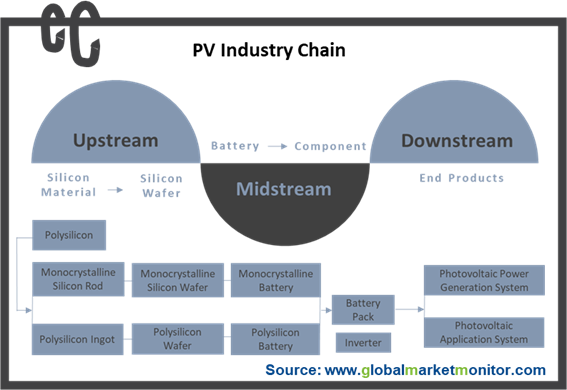

The photovoltaic industry chain is long and complex. The upstream is the link of silicon materials and wafers; the middle is the link of solar cells and battery modules; the downstream is the link of application systems. From a global perspective, the number of companies involved in the upper, middle, and downstream links of the industrial chain has increased substantially, and the photovoltaic market industrial chain has a pyramidal structure.

Enquire before purchasing this report-

https://www.chinamarketmonitor.com/request.php?type=3&rid=267206

Polycrystalline silicon material is the basic raw material for the information industry and solar cell industry, which is refined from metallurgical-grade silicon processed from quartz sand and used to manufacture crystalline silicon-based battery modules. Polycrystalline silicon wafers have certain cost advantages over monocrystalline silicon wafers. The silicon material industry has a high threshold, with a serious foreign monopoly. With the success of the independent technology research and development in China, it has now got rid of import dependence.

The Recent Rise in the Price of Polysilicon Materials Increases Confidence in the Later Resumption of Production

Last week, the price of polysilicon materials rose and 5%, and the price of silicon materials rose sharply. The price increase contains many factors.

There was an accident in the rectification workshop of a silicon material enterprise polysilicon project in Xinjiang in early July, which will affect the production progress and accelerate the rise of silicon material prices; in addition, Xinjiang has recently appeared A round of new crown cases. From July 15 to July 19, 47 cases have been confirmed. The region has shifted its focus from restoring social and economic development to epidemic prevention. Although overall production will not be greatly affected, it will cause emotional fluctuations in the market in a short period of time. Due to the drop in silicon material prices in the early stage, there are still 3 silicon material manufacturers performing overhaul or equipment maintenance to reduce load production in July, and silicon material production capacity is also increased but still Insufficient. The resumption of production can only be accelerated after the subsequent silicon material price rises significantly.

The Backward Production Capacity Is Gradually Withdrawn, And the Industry Competition Pattern Is Optimized

Two years back, silicon material prices in China have been in a slow decline since the second half of 2018.

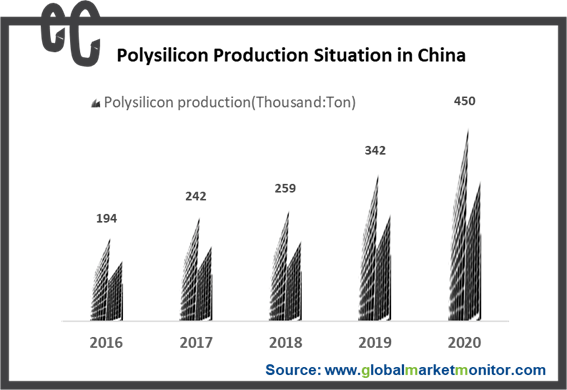

2019 is the peak of domestic silicon production, in which the domestic new silicon material production capacity released exceeded 150,000 tons, a year-on-year increase of more than 50%, mainly including 35,000 tons of Tongwei Baotou, 35,000 tons of Tongwei Leshan, and 35,000 tons of Xinte Phase II, and large new production capacity 35,000 tons. The production capacity is faster than the growth of terminal demand and the release of monocrystalline silicon wafer production capacity.

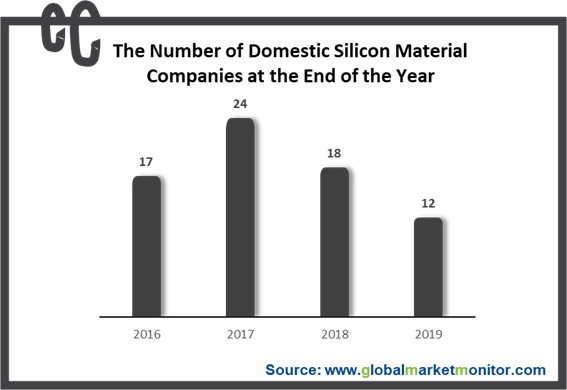

The large expansion of the production capacity of the above five companies has affected the supply and demand pattern of the global polysilicon industry. Under the impact of large-scale, low-cost silicon material production capacity, industrial integration is rapidly advancing, and companies that are not competitive are accelerating their exit. According to statistics, 6 polysilicon companies have ceased production for maintenance throughout 2019. The number of domestic polysilicon companies in production has decreased from 24 at the beginning of 2018 to 18 at the beginning of 2019, and then reduced to 12 at the end of 2019.

For the whole year of 2019, the output of the top five silicon materials companies reached 77.8%, a significant increase from 60.5% in 2018. It is expected that some relatively backward production capacity will be withdrawn further in 2020, and the production capacity of the top five is expected to reach 84%.

The Global Production Center Shifts to China, with Higher Industry Concentration

In 2020, there are 15 global production companies with a production capacity of approximately 660,000 tons and an output of approximately 250,000 tons, in which 11 companies are located in China, with an effective production capacity of 466,000 tons and an output of 205,300 tons.

At present, the total production capacity of the world's top ten polysilicon producers has reached 552,000 tons, accounting for 81.8%. Among the top 10, China accounts for 7 seats, which can be seen that the global polysilicon production center shifts to China.

In China, the focus of polysilicon production has further shifted to Xinjiang and Inner Mongolia. It is expected that the production capacity of the two places will account for 52% of the world’s share by the end of this year; at the same time, polysilicon production capacity has also further concentrated, with the top five production capacity reaching 488,000 tons, accounting for 87.3% of total production capacity of China.

Besides, the production of foreign polysilicon companies is not optimistic. REC and Hemlock have exited the top ten. OCI announced plans to close its two solar-grade polysilicon factories operating in South Korea, retaining part of the production of electronic-grade polysilicon, and minimizing its South Korean production. Production of solar-grade polysilicon materials. The exit of OCI provides a 10% shortfall in the supply of solar polysilicon, and the remaining advantageous companies will further occupy the market and the industry concentration will further increase.

The Demand Market Has Broad Prospects and the Industry Leaders Concentrate Their Profits

In terms of demand in the second half of the year, global silicon wafer production is expected to be about 77GW, polysilicon consumption is 250,000 tons, of which domestic silicon wafer production is about 74GW, and polysilicon consumption is 240,000 tons.

As a renewable energy source, the penetration rate of photovoltaics is a general trend. Global photovoltaic power generation will account for 18.7% of total power generation in 2040. In 2018, the global penetration rate of photovoltaic power generation was only 2.2%. In 2019, China's photovoltaic power generation penetration rate will increase to 3.1%. The market space for photovoltaic power generation broad.

The pattern of silicon materials is optimized, the leading companies are expanding production against the trend, the outdated production capacity is cleared, and the pattern of oligarchs is clear. Global photovoltaic demand will improve in 2020, and the growth rate of silicon material demand will increase 18%, but the new capacity on the supply side is limited or even slightly contracted. The supply-demand relationship of silicon materials is expected to reverse, and the price of silicon materials may increase by 25%. Leading companies are expected to benefit collectively by releasing their production capacity and increasing their shipments, cost reduction and price increase. Recommended first-line leaders in silicon materials: Tongwei and Daquan New Energy.

LEARN MORE:

Electronic Grade Polysilicon

https://www.chinamarketmonitor.com/reports/377414-electronic-grade-polysilicon-market-report.html

Solar Photovoltaic

https://www.chinamarketmonitor.com/reports/267206-solar-concentrated-photovoltaic-market-report.html