Photovoltaic III: Solar Cells

When the energy issue has increasingly become a bottleneck restricting international social and economic development, more and more countries are developing solar energy resources to seek new impetus for economic development. Driven by the huge potential of the international photovoltaic market, solar cell enterprises in various countries are vying to invest heavily in expanding production to compete for a place.

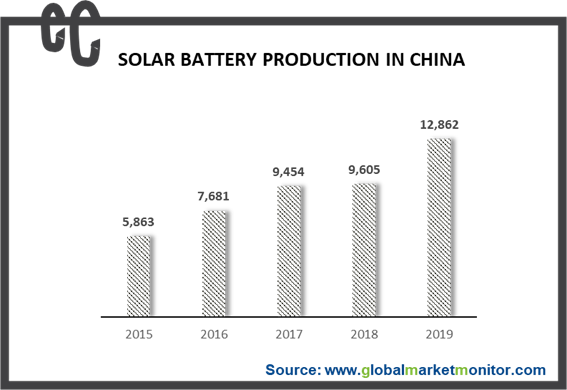

At present, the global solar cell market is fiercely competitive, the leading pattern in Europe and Japan has been broken, and the production center of solar cell has been transferred to Asia. In 2019, solar cell production in China accounted for 83% of global production, with an output of 128.62 million kilowatts, a year-on-year increase of 33.9%.

The solar cell is a device that uses the photovoltaic effect to directly convert solar energy into electrical energy. The development of solar cells has mainly experienced three technological development routes, including BSF batteries, and PERC batteries and N-type batteries, among which the new technology routes for N-type single crystals include PERT, HJT, and IBC, and other routes. At present, PERC battery is still the mainstream batterytechnology, and the HIT is a new process technology. In recent years, the competition between these two batteries has been fierce.

Enquire before purchasing this report-

https://www.chinamarketmonitor.com/request.php?type=3&rid=370997

Since the development of the photovoltaic industry, efficiency and cost have always been the keywords for industrial development. Solar energy has low energy density and high collection cost, which determines that the most important way to reduce the cost of photovoltaic power generation is to improve the conversion efficiency of modules. For every 1% increase in module conversion efficiency, the cost of photovoltaic power generation can be reduced by more than 6%.

Under the industry trend of reducing costs and increasing efficiency, what is the gap between the mainstream PERC battery and the new process line HIT at this stage?

Comparison of PERC Battery, HIT Battery and IBC Battery

In terms of efficiency, HIT batteries have significant advantages. Due to the high open-circuit voltage of HIT battery, its theoretical efficiency is as high as 27%, which is at the forefront of the current technical route, while that of the PERC potential is expected to be 23%. Currently, the laboratory efficiency of HIT batteries is above 26%, and the average mass production efficiency of existing facilities is above 23%.

In the field of cost, HIT cells combine the advantages of low-temperature manufacturing of thin-film solar cells, avoiding traditional high-temperature processes. The low-temperature processing environment is conducive to the realization of HIT cell thinning, which not only greatly saves fuel energy, but also reduces silicon usage and silicon Raw material costs. At present, PERC batteries need to use about 180um silicon wafers (the industry target is 80um) due to multiple high-temperature processes. The thinner the thickness, the smaller the silicon consumption and the lower the silicon cost. Besides, the HIT process is relatively simplified, and the entire production process is only It takes four steps to complete. While the process steps are as many as 8 steps of PERC cells to achieve a 23.9% conversion efficiency, which brings higher costs.

The ultra-low attenuation and long life of the HIT battery. And the low-temperature coefficient and lower light-induced attenuation of the HIT battery, make the stability high and effectively reduce the heat loss. The power generation of modules of the same wattage can be 8%-10% higher than that of PERC monocrystalline. HIT cells can also be packaged with double glass to extend the life span of 5-15 years compared with the current mainstream modules of 25 years.

And for IBC batteries. The technological process is much more complicated than traditional methods, which requires twenty process steps. IBC also has higher requirements for silicon wafers, and the complicated steps have resulted in its cost approximately twice that of ordinary batteries, and its industrialization progress is also very slow. Because the front and back of IBC are different from the conventional one, its component process also needs to be customized, which also restricts its industrialization.

In the future, IBC batteries are mainly targeted at the high-end market. The advantage of the IBC battery lies in its high efficiency and good shape, while its disadvantage lies in its complexity and cost with the difficulty to reduce compared with HIT batteries. Besides, its battery and module production capacity must be matched, resulting in excessive investment costs, and the progress of industrialization will be slower.

Therefore, the HIT battery has become the industry-recognized ultimate solution for future battery technology due to its high photoelectric conversion efficiency, excellent performance, and good prospects for affordable Internet access.

In general, HIT battery refers to a crystalline silicon heterojunction solar cell, which is a silicon solar cell with a HIT structure. The HIT structure is to deposit a layer of non-doped (intrinsic) hydrogenated amorphous silicon film and a layer of a doped hydrogenated amorphous silicon film with the opposite doping type of crystalline silicon, which are the reason that the conversion efficiency reaches 23%, the open-circuit voltage reaches 729mV, and the entire process can be achieved below 200°C.

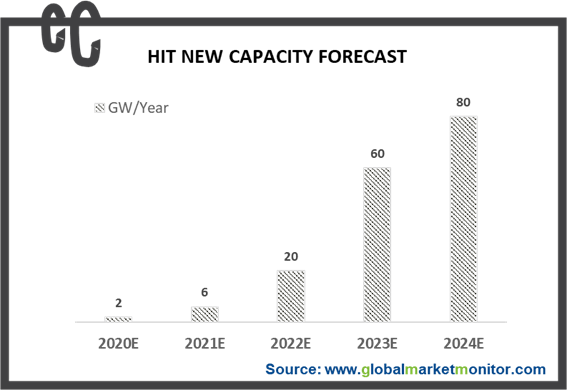

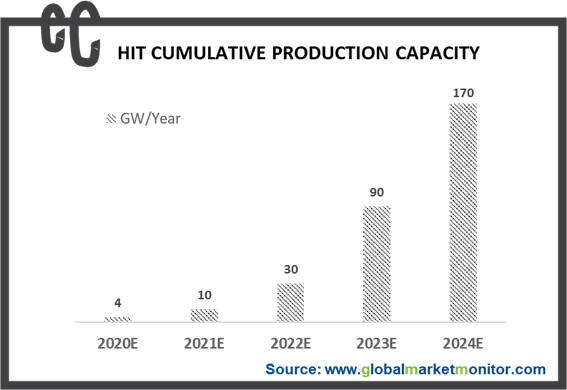

2020 May Be the First Year of HIT's Industrialization.

With high-quality power generation performance and the huge potential of HIT batteries, it has ushered in investment from various capital markets.

In May 2019, Jinneng Technology announced in Chengdu that the average efficiency of the company's innovative HJT battery has reached 23.79%, with the highest efficiency of 24.73%.

In July 2019, Fujian GS-SOLAR and Shanxi Coal International Energy Group, the two parties will jointly build an HDT production base of up to 10GW.

In August 2019, 2.5GW high-efficiency heterojunction battery and module production project of Ningbo Risen started, with a total investment of 3.3 billion yuan and an area of approximately 205 acres.

In March of this year, Jiangsu Akcome announced that 1.19 billion of the raised funds will be used for battery and component projects.

The Large-Scale Industrialization of HIT Batteries Is by No Means Smooth

The high cost is the biggest restriction in the promotion of heterojunction technology, and the high cost stems from the disparity between equipment investment and output.

Key equipment with a high cost of operation maintenance has not been localized. The imported HIT battery equipment is about 800 million to 1 billion yuan/GW, while domestic equipment is about 500 to 800 million yuan/GW, and PERC only needs 250 to 300 million yuan/GW, in which the cost of HIT battery equipment is about 3 times that of PERC, and the investment per unit capacity is 2-4 times that of the PERC production line. Also, the lack of supporting and professional equipment has led to low battery yields and high operation and maintenance costs as HIT has just started in China.

Besides, the material cost is high, the output is small without scale effect, and the quality and price of silicon wafers and auxiliary materials are high. The high-quality N-type silicon wafers required by HIT batteries are expensive. The unit price of low-temperature silver paste required by the process is about 1.5 times that of PERC silver paste, and the amount is 1.5 times that of PERC.

Scale is one of the main paths for equipment cost reduction and localization is also expected to significantly reduce equipment costs. Currently, domestic equipment is entering, with some companies such as Shenzhen S.C and Fujian GS-SOLAR which have product capabilities in different links of cleaning, TCO, and screen printing. As domestic equipment matures, the cost of HIT equipment is expected to be greatly reduced, resulting in the reduction of the HIT battery price.

HIT technology is limited by the high cost. However, many companies in the industry in the global market vigorously deploy heterojunction technology, and the pace of commercialization of heterojunction is expected to accelerate.

LEARN MORE:

Solar Cells and Modules

https://www.chinamarketmonitor.com/reports/370997-solar-cells-and-modules-market-report.html

Solar Photovoltaic

https://www.chinamarketmonitor.com/reports/267206-solar-concentrated-photovoltaic-market-report.html